Sen. Mark Warner introduces legislation for students struggling with debt

BY LAURYN CANTRELL

Senator Mark Warner (D-Va.) has introduced two bills to assist college students and college graduates in response to the rising cost of attending college.

In a phone conference with student journalists from Virginia universities, including Mason, Warner highlighted how the two bills will help graduates with their student loans.

“This is an issue [students] are living… If I had had that much debt coming out of college, I’m not sure I would be sitting where I am right now,” Warner said.

The basis of the two bills, the Dynamic Repayment Act and the Employer Participation in Repayment Act, are founded on a common-sense, income-based repayment system, according to Warner.

Introduced by Warner and Sen. Marco Rubio (R-Fla.), the bill has been years in the making, but Warner said he hopes its bipartisan support will make it more likely to pass.

“Marco Rubio and I are the firsts in our family to graduate from college, and we asked ourselves what were our aspirations and what could we do that could actually pass a Senate that is currently not getting much done,” Warner said.

The Dynamic Repayment Act seeks to simplify the current income-driven payment system, which outlines how much a grad student is obligated to save to pay their student loans based on how much income they take in. The bill proposes to combine federal student loan options, such as subsidized Stafford loans, unsubsidized Stafford loans and Grad PLUS loans, into a single loan repaid through an income-based system.

“It helps students during those first few years coming out of college to give you more freedom and stability,” Warner said.

The act does not create an additional option on top of other existing plans; rather, it restructures current payment options into a simple plan automated to adjust to changes in a borrower’s income, according to Warner.

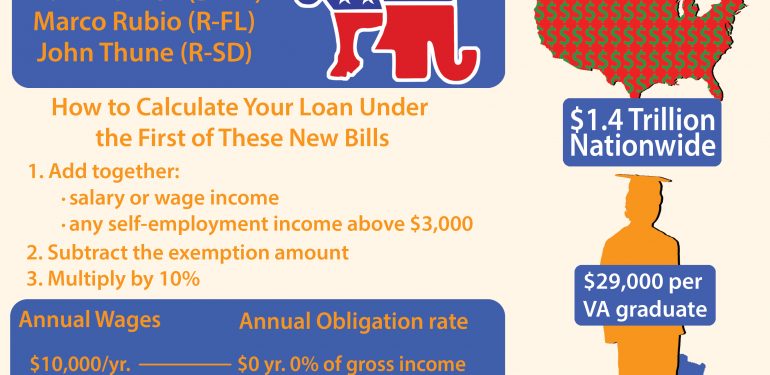

Warner added that a borrower will be obligated to pay 10 percent of their income above the $10,000 exemption amount. For example, a borrower making an annual salary of $40,000 would pay 10 percent of $30,000, according to a press release from the office of Sen. Mark Warner (D-Va.). If an individual makes less then $10,000, then they are excused from paying taxes in accordance with the current progressive U.S. tax system. If the exemption is a greater share of a low-pay individual’s income, the current tax rate for their income will be used to determine the person’s obligated loan payment.

If a balance of $57,500 or less remains after 20 years of paying student loans, the student will be forgiven of their remaining debt and will not owe the remaining sum, according to the bill’s legislative summary by the offices of Sen. Warner (D-Va.) and Sen. Rubio (R-Fla.).

“Student loan debt currently stands at nearly $1.4 trillion nationwide, outdoing credit card debt and auto insurance,” Warner said.

The average Virginia public university student will graduate with $29,000 in student debt, according to the Student Loan Report.

A January 2017 study conducted by the Consumer Financial Protection Bureau stated, “The number of consumers age 60 and older with student loans has quadrupled over the last decade in the United States, and the average amount they owe has also dramatically increased.”

Due to a continuing increase in tuition and cuts in state funding cuts for public universities, the newest college graduates face carrying their student debt later in life, according to a 2015 report from USA Today College.

As of writing this article, there is no set date for the implementation of the Dynamic Repayment Act.

The second bill, which Warner introduced with Sen. John Thune (R-SD), is the Employer Participation Repayment Act (OTT17138), which amends the Internal Revenue Code of 1986, allowing employers to pay for students’ tuition, Warner said. The revision to the act will include assistance in paying student loans as an employer-provided benefit.

“If [a student] were to drop out of college and work for a company, an employer could send them back to school and help pay for their continuing education,” Warner said. “We want to equalize the benefit for sending somebody back to school and someone graduating from school with debt.”

Employers will be allowed to contribute up to $5,250 in deductible pre-tax dollars to their employee’s loans, according to the bill. If passed, The Employer Participation in Repayment Act of 2017 will apply to payments made after Dec. 31, 2017, as explained in the bill.

Both of these new reforms only affect federal student loans provided by the Free Application for Federal Student Aid (FAFSA), not private student loans, Warner said. This includes direct subsidized loans, direct unsubsidized loans, direct PLUS loans and federal Perkins loans. Neither proposal reduces college costs, for that is an even larger, more progressive issue to act on, Warner said.

“Given the current administration, it is going to be hard to push the more progressive, so what we [the co-sponsors] are focused on are two pieces of legislation that have a greater chance [of passing] this year… but I do believe this year we will see some action on these bills.”

For more information on the acts, go to Warner’s website at warner.senate.gov/public.